Unit 2.1 - Demand, Supply and Market Equilibrium

Demand

Concept of Demand

Demand is defined as the effective desire for a good or service backed by ability and willingness to pay. It is also defined as the quantity of a good or service which a consumer would buy in a market at a given price and time period.

Demand Function

The demand for a particular commodity is influenced by so many factors-they together are known as determinants of demand in technical jargon. A demand function in mathematical term expresses functional relationship between the demand for a product and its various determining factors. For instance,

Qdx = f(Px, Py, Y, Adv, T&P, F, Cl, Pop, Gp, Exp., Dist. ......)

Types of Demand Function

1. Short Run Demand Function: Qdx = f(Px) ...........OTRS

2. Long Run Demand Function: Qdx = f(Px, Py, Y, Adv, T&P, F, Cl, Pop, Gp, Exp., Dist., ......)

3. Linear Demand Function: The slope of the demand curve remains constant throughout its length is known as LDF. In other words, if both independent and dependent variable changes at a constant rate, the demand function will be linear.

4. Non-Linear Demand Function: A demand function is said to be non-linear when the slope of a demand curve changes all along the demand curve. If both dependent and independent variable generally expressed in power function as follows:

Video Link: Concept of Demand and Demand Function

Types of Demand

Demand is generally classified on the basis of various factors, such as nature of a product, usage of a product, number of consumers of a product and suppliers of a product. Some types of demand are as follows:

1] Price Demand: The price demand means the amount of commodity a person is willing to purchase at a given price. OTRS, there is inverse relationship between price and demand for the same commodity.

2] Income Demand: Income demand refers to the willing of an individual to buy a certain quantity at a given income level, OTRS. There is direct or positive relationship between income and demand for normal/superior goods. But, in case of inferior goods (low quality goods), there is inverse or opposite relationship between income level and quantity demand.

3] Cross Demand: When the demand for a commodity depends not on its price but on the price of other related commodities, it is called cross demand. There is positive relationship between quantity demand of one commodity and price level of another substitute commodity (competitive goods) i.e. Samsung Tab and Apple - iPad. But, in case of complementary goods, there is inverse relationship between quantity demand of one commodity and price level of another commodity i.e. car and petrol.

4] Joint Demand: Quantity demand for several goods by a consumer to fulfill their single purpose (as a finished goods/final product) is known as joint demand. For e.g. to prepare a cup of coffee, we some goods like sugar, milk, coffee powder and water. Similarly, for the construction of a house we require land, capital, organization and materials like cement, bricks, lime etc.

5] Composite Demand: If a commodity or service can fulfill several needs, it is called composite demand. For e.g. demand for a tomato can be used to make the pickle, curry and soup. Similarly, demand for milk, coal and electricity for the several uses are the composite demand.

Video Link: Types of Demand

Determinants of Demand

We already know that in short-run the basic dependency of demand is the price of the same commodity. But in the long-run there are some other factors which also affect demand. This dependency of demand on various factors is described as demand function which can be expressed as,

Qdx = f(Px, Py, Y, Adv, T&P, F, Cl, Pop, Gp, Exp., Dist., ......)

The response of demand to each of these factors can be discussed in detail as follows:

1] Price of the Product (Px): People used price as a parameter or fundamental determinant to make decisions if all other factors remains constant or equal. According to to the law of demand, this implies an increase in demand follows a reduction in price and decrease in demand follows an increase in the price of same goods. If the quantity demanded responds a lot to price, then it's known as elastic demand. If the volume doesn't change much, regardless of price, that's inelastic demand.

2] Income (Y): The income of a consumer affects his/her purchasing power, which, in turn, influences the demand for a product.

a. Essential or Basic Consumer Goods: Refer to goods that are consumed by all the people in the society. For e.g. food grains, soaps, oil, cooking fuel and clothes. A rise in a person's income will lead to an increase in demand to certain limit, a fall will lead to a decrease in demand for normal goods.

b. Inferior Goods: Goods whose demand varies inversely with income are called inferior goods. For e.g. a consumer would prefer to purchase wheat and rice instead of millet and cooking gas instead of firewood, with increase in his/her income. In such case, millet and firewood are inferior goods to the consumer with the rise in income.

c. Luxury Goods: Refers to those pleasure goods, whose demand increases with the rise in income level of the consumer. For e.g. expensive jewelry items, luxury cars, antique painting, furniture and wines, air travelling etc.

3] Price of Related Goods (Py): The demand for one specific product is influenced by the price of another product to a greater extent, are known as related goods.

a. Substitute Goods: Substitute goods are those goods, which can be used to replace each other. Price of one good is positively related to the demand for another substitute goods. For e.g. tea and coffee.

b. Complement Goods: Complement goods are those goods, which can be used together. Price of one goods is inversely related to the demand for another complement goods. For e.g. pen and ink.

4] Taste and Preferences of Consumer (T&P): The taste and preferences of the consumers are affected by various factors like life style, customs, common habits, influence in advertising, standard of living, changes in fashion (old to new), religious values, age, gender (make-up kits or cosmetics) and so on. A change in any of these factors leads to change in the tastes and preferences of consumers. Any favorable change in taste and preferences of consumer leads to an increase in demand and vice-versa.

5] Consumer's Expectations (Exp.): When people expect that the value of some will rise, they demand more of it.

a. Future Price: Consumer's current demand will increase if they expect higher future prices because of taxation policy, their demand will decrease if they expect lower future prices for non-essential products because of over production.

b. Future Income: Consumer's current demand will increase if they expect higher future income and vice-versa.

c. Scarcity of goods: Scarcity of specific products in future would also lead to an increase in their demand in present.

6] Number of buyers or population (Pop.): The number of consumer affects overall or aggregate demand. As more buyers enter the market, demand rises without change in price and vice-versa.

7] Advertisement (Adv.): Effective advertisements are helpful in many ways, such as catching the attention of consumer, informing them about the availability of a product, demonstrating the features of the product to potential consumers, and ultimately persuading them to purchase the product. More expenditure on attractive advertisement through several celebrities may help to boost the demand for the product.

8] Distribution of Income in the Society (Dist.): When income is fairly distributed among people in the society, the demand for products is higher and vice-versa. Similarly, demand for different types of goods also depends on the different income segment in the society. For e.g. the high income segment of the society would prefer luxury goods, while the low income segment would prefer necessary goods.

9] Government Policy (Gp): If a product has high tax rate, this would increase the price of the product and this would lead to decrease in demand. On the other hand, if the subsidy and credit facility is available to citizens by the government, this would induce the the demand.

10] Climate Condition(Cl.): The demand of ice-creams and cold drinks increase in summer, while tea and coffee are preferred in winter.

Video Link: Determinants of Demand

Law of Demand

Introduction

Law of demand is one of the popular, important and most applied theories of microeconomics, propounded by Alfred Marshall in his book "Principles of Economics" published in 1890 A.D. The law of demand expresses an inverse relationship between the quantity demanded and its price. It may be defined in Marshall's words as "the amount demanded increases with a fall in price, and diminishes with a rise in price".

The law refers to the direction in which quantity demanded changes with a change in price. On the figure, it is represented by the slope of the demand curve which is normally negative throughout its length.

Mathematically, the law of demand can be expresses as: Qdx = f(Px), ceteris paribus

As price and quantity demand are inversely related in mathematical notation this is expressed as

ΔP/ΔQdx<0.

The inverse price-demand relationship is based on other things remaining same. This phrase points towards certain important assumption on which this law is based.

Assumptions

- The income of the consumer remains constant;

- No change in price of related goods;

- There is no change in the taste and preferences of the consumer;

- No change in climate;

- No change in size and composition of population;

- No expectation of change in future price of the commodity and income of the consumer;

- No change in advertisement expenditure;

- There should not be any change in the quality of the product;

- The fashion and habits of the consumers should remain unchanged.

Given these conditions, the law of demand operates. If there is change even in any assumption, it will stop operating.

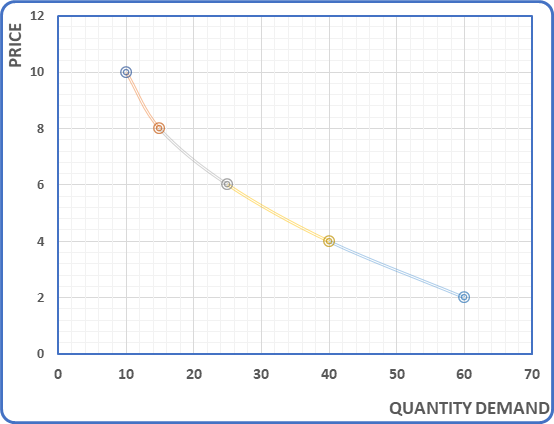

Explanation with Table and Diagram

Exceptions or Limitations of the Law of Demand

The situations, in which the law of demand does not hold true considered as limitations of law of demand. Under certain circumstances, the demand curve slopes upward from left to right i.e. it has a positive slope. Many causes are attributed to an upward sloping demand curve. Some are as follows:

1] War: If shortage is feared in anticipation of war, people start buying more for building stocks or for hoarding even when the price rises.

2] Depression: During a depression, the prices of commodities are very low and the demand for them is also less. This is due to the lack of purchasing power with consumers.

3] Giffen Paradox: A Giffen good is a low income, non-luxury product for which demand increases as the price increases and vice-versa. Demand for Giffen good is heavily influenced by a lack of close substitute and income pressures. For e.g. demand for bread increases when its price level increases because poor people lacked the income to buy meat. This is what Marshal called Giffen paradox which makes the demand curve to have a positive slope.

4] Demonstration Effect: Demonstration effect means change in demand of the product due to purchase pattern in the society. In the presence of demonstration effect, demand for the product like diamond increases whether price of that price is higher than before.

5] Ignorance Effect: In case of irrational consumer, he/she may demand more with the rise in price of the product due to deceptive packaging and label, etc.

6] Necessities of Life: Even the price of necessary goods like food, medicine, cloth increases, consumer does not reduce their demand.

7] Natural Calamities: Due to the low production and shortages of goods in the market at the time of natural calamities, demand may not reduce even at the higher price.

If other things does not remain same, the law of demand does not hold true means there may be positive relationship between price level and quantity demand of the same produce.

Video Link: Law of Demand

Reason for Downward Sloping Demand Curve

The inverse relationship between quantity demand and price is reflected in the downward sloping demand curve because of some reasons. Some are summarized as follows:

1] Law of Diminishing Marginal Utility: With the additional consumption of same product, marginal utility or additional satisfaction level falls, hence consumers are prepared to pay less for additional demand. Because rational consumer always try to equalize marginal utility with price. If price of the product becomes smaller than than utility, then consumer demand more to equalize utility with price.

2] Income Effect: If price of the commodity changes, purchasing power also changes with the same level of income or expenditure amount. Normally, purchasing power increases when price of the product falls and vice-versa. With the rise in real income due fall in price, consumer may demand more of that commodity.

3] Substitution Effect: Consumers have a tendency to shift to cheaper commodities when the price of a commodity increases. This results in reduction in demand of the expensive commodity. For e.g. with the rise in price of coffee, the demand for tea increases. It means demand for coffee reduces with the rise in price because of the availability of substitute goods tea.

4] Entry of New Consumers: Those who did not consume when the price went up, now if the price goes down they also start consuming. That is, when prices fall, demand increases as new consumers arrive.

5] Psychological Effect: People often have a psychological state of buying more at a lower price and consuming less at a higher price, which creates an inverse relationship between price and demand.

6] Multiple use of a Product: In the case of multipurpose goods, if the price goes down, the demand for the commodity for various uses will increase, not limited to the important use of the commodity. Such as electricity, water, potatoes, etc.

Video Link: Reason Behind Downward Sloping Demand Curve

Individual and Market Demand Schedule and Curve

Demand Schedule

Demand Schedule is a tabular presentation showing different quantities of a commodity that would be demanded at different prices.

Demand Curve

The graphical representation of demand schedule is called a demand curve. It is of two types:

Video Link: Individual and Market Demand Schedule and Curve

Change in Demand Curve

Quantity demand of goods and services may influence by various determinants like price factors and non-price factors and it results in change in demand curve. The change in demand curve can be analyzed in two ways:

Movement along the Same Demand Curve

Comments

Post a Comment

If you have any doubt, Please let me know !